Understanding Fractional Banking: A Comprehensive Guide

Fractional banking is a fundamental concept in modern economics that plays a crucial role in how money supply is managed and how financial institutions operate. In this article, we will delve into the intricacies of fractional banking, exploring its mechanisms, benefits, challenges, and its impact on the economy. Understanding fractional banking is essential for anyone interested in finance, economics, or how monetary systems function.

As we unpack this topic, we will look at the historical context of fractional banking, the principles that govern it, and its implications for both banks and consumers. Moreover, we will examine how this banking system affects the broader economy and the potential risks involved. By the end of this article, you will have a solid foundation in fractional banking and its significance in today’s financial landscape.

Whether you are a student, a professional in the finance sector, or simply a curious individual looking to expand your knowledge, this guide aims to provide valuable insights into fractional banking. Let's begin our exploration of this fascinating subject.

Table of Contents

- What is Fractional Banking?

- History of Fractional Banking

- How Fractional Banking Works

- Benefits of Fractional Banking

- Risks and Challenges

- Impact on the Economy

- Regulations and Oversight

- Future of Fractional Banking

What is Fractional Banking?

Fractional banking refers to the banking system in which banks are required to keep only a fraction of their deposits in reserve, while they can lend out the rest. This system allows banks to create money through lending, effectively expanding the money supply in the economy.

In fractional banking, the reserve requirement is determined by the central bank and varies by country. For instance, if the reserve requirement is set at 10%, a bank holding $1,000 in deposits must keep $100 in reserve and can lend out $900.

This process of lending and re-lending creates a multiplier effect, where the initial deposit leads to a more significant amount of money circulating in the economy. As loans are made and deposited back into banks, more money can be lent out, leading to economic growth.

History of Fractional Banking

The concept of fractional banking dates back to the medieval period when goldsmiths began issuing receipts for gold deposits. These receipts functioned as money, allowing individuals to make transactions without physically exchanging gold.

Over time, banks began to realize that not all depositors would withdraw their funds simultaneously. This realization led to the establishment of the fractional reserve system, where banks could lend out a portion of their deposits while retaining enough reserves to meet withdrawal demands.

Significant milestones in the history of fractional banking include the establishment of central banks, which regulate reserve requirements and oversee banking operations to maintain financial stability.

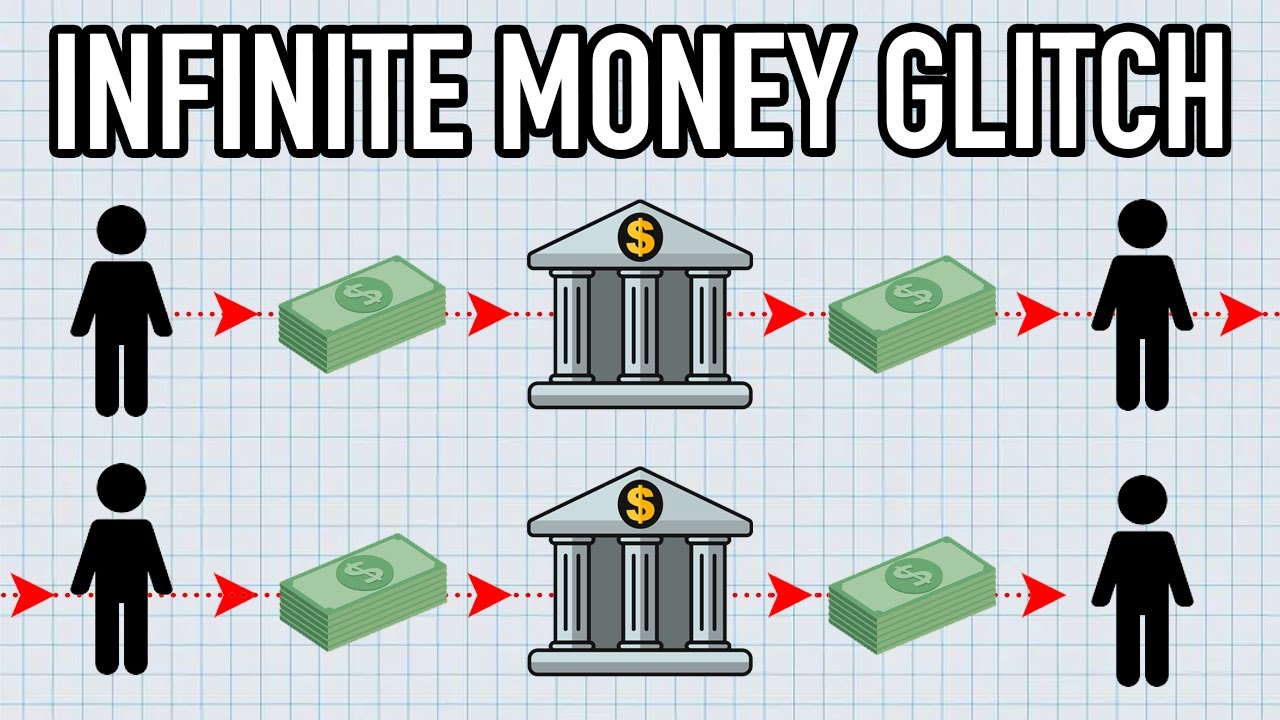

How Fractional Banking Works

The mechanics of fractional banking involve several key steps:

- Deposit: A customer deposits money into a bank account.

- Reserve Requirement: The bank holds a fraction of the deposit as reserves, as mandated by the central bank.

- Lending: The bank lends out the remaining funds to borrowers, charging interest.

- Money Creation: As borrowers spend the loaned money, it circulates in the economy, and some of it is deposited back into banks.

- Repeat: The cycle continues, creating more money in the economy.

Example of Fractional Banking

To illustrate fractional banking, consider the following example:

- Initial Deposit: $1,000

- Reserve Requirement: 10%

- Reserves Held: $100

- Funds Available for Lending: $900

When the bank lends out $900, that money may be deposited by the borrower in another bank, allowing that bank to lend out 90% of it, and so on. This creates a potential total money supply of $10,000 from the initial $1,000 deposit, demonstrating the power of fractional banking.

Benefits of Fractional Banking

Fractional banking provides several advantages:

- Economic Growth: By allowing banks to lend more money than they hold in deposits, fractional banking stimulates economic activity and growth.

- Increased Money Supply: This system enables the money supply to expand, which can lead to lower interest rates and increased borrowing.

- Flexibility: Financial institutions can respond to the needs of the economy by adjusting their lending practices and reserve levels.

- Investment Opportunities: Borrowers can access funds for investments, education, and other purposes that contribute to personal and economic development.

Risks and Challenges

Despite its benefits, fractional banking is not without risks:

- Bank Runs: If too many depositors withdraw their funds simultaneously, a bank may not have sufficient reserves to cover withdrawals, leading to a bank run.

- Credit Risk: When banks lend to borrowers who may default, it increases the risk of financial instability.

- Inflation: Excessive lending can lead to inflation if the money supply grows faster than the economy's ability to produce goods and services.

- Systemic Risk: The interconnectedness of banks can create systemic risks, where the failure of one bank can impact others.

Impact on the Economy

Fractional banking plays a significant role in shaping economic conditions:

- Monetary Policy: Central banks use reserve requirements to regulate the money supply and influence interest rates, impacting economic growth and inflation.

- Consumer Spending: Access to credit encourages consumer spending, which drives demand for goods and services.

- Investment: Businesses can secure loans for expansion, innovation, and job creation, contributing to economic development.

Regulations and Oversight

The fractional banking system is subject to regulations to ensure stability and protect consumers:

- Reserve Requirements: Central banks impose minimum reserve requirements to ensure banks maintain sufficient liquidity.

- Capital Adequacy: Regulations require banks to hold a certain amount of capital to absorb losses and reduce systemic risk.

- Consumer Protections: Laws are in place to protect consumers from unfair lending practices and ensure transparency.

Future of Fractional Banking

The future of fractional banking may be influenced by several factors:

- Technological Advancements: Innovations in fintech may change how banks operate, with potential impacts on lending and reserve management.

- Cryptocurrency: The rise of cryptocurrencies could challenge traditional banking models, leading to new forms of money and payment systems.

- Regulatory Changes: Ongoing changes in regulations may reshape the landscape of fractional banking.

Conclusion

In summary, fractional banking is a vital component of modern financial systems that facilitates economic growth and development. While it presents certain risks, effective regulations and oversight can help mitigate these challenges. As we move forward, understanding fractional banking will remain essential for navigating the complexities of the financial world.

We encourage you to share your thoughts in the comments below, explore other articles on our site, and stay informed about the dynamic world of finance.

Final Thoughts

Thank you for taking the time to read our comprehensive guide on fractional banking. We hope you found the information useful and informative. Remember to bookmark our site for more articles that will enhance your understanding of financial concepts and practices.

SMCI Stock Forecast: An In-Depth Analysis For Investors

Delicious And Authentic Italian Dressing Recipe: A Culinary Delight

Lexus RX 350 Used: A Comprehensive Guide For Buyers

:max_bytes(150000):strip_icc()/fractionalreservebanking.asp-final-a5faeb741c464711ba434ee652c40ebf.png)

{kind=link}