Calculate House Payment: A Comprehensive Guide To Understanding Your Mortgage Costs

When it comes to buying a home, understanding how to calculate house payment is crucial for any potential homeowner. The mortgage payment is often one of the largest monthly expenses for families, making it vital to grasp how various factors influence it. From the principal and interest to taxes and insurance, knowing how to compute these costs can help you make informed financial decisions and avoid any unpleasant surprises.

In this comprehensive guide, we will delve into the various components involved in calculating your house payment, including practical tips and resources to assist you in managing your mortgage effectively. Whether you are a first-time homebuyer or looking to refinance, this article will provide valuable insights that can empower you to take control of your financial future.

By the end of this article, you will not only understand how to calculate your house payment but also gain insights into mortgage types, interest rates, and additional costs that come with homeownership. Let's get started on this journey to financial literacy!

Table of Contents

- What is House Payment?

- Components of House Payment

- How to Calculate House Payment

- Types of Mortgages

- Understanding Interest Rates

- Additional Costs Associated with Homeownership

- Tips for Managing Your Mortgage

- Conclusion

What is House Payment?

A house payment refers to the total monthly cost associated with repaying a mortgage loan. This payment typically includes several components:

- Principal: The original loan amount borrowed.

- Interest: The cost of borrowing the principal amount.

- Property Taxes: Local government taxes based on the property’s assessed value.

- Homeowners Insurance: Insurance that protects against damages to the home.

- Private Mortgage Insurance (PMI): Required if the down payment is less than 20%.

Components of House Payment

Understanding the components of your house payment is essential for accurate calculations. Here’s a breakdown of each element:

1. Principal

The principal is the amount of money you borrow from a lender to buy a home. Reducing this amount can directly lower your mortgage payment.

2. Interest

Interest is the fee charged by the lender for borrowing money. This is usually expressed as an annual percentage rate (APR).

3. Property Taxes

Property taxes are levied by local governments and can vary significantly based on location. These taxes are typically included in your monthly payment and are held in an escrow account.

4. Homeowners Insurance

This insurance covers damages to your home and protects against liability in case of accidents. It is often required by lenders.

5. Private Mortgage Insurance (PMI)

If your down payment is less than 20%, you might have to pay PMI, which protects the lender in case you default on the loan.

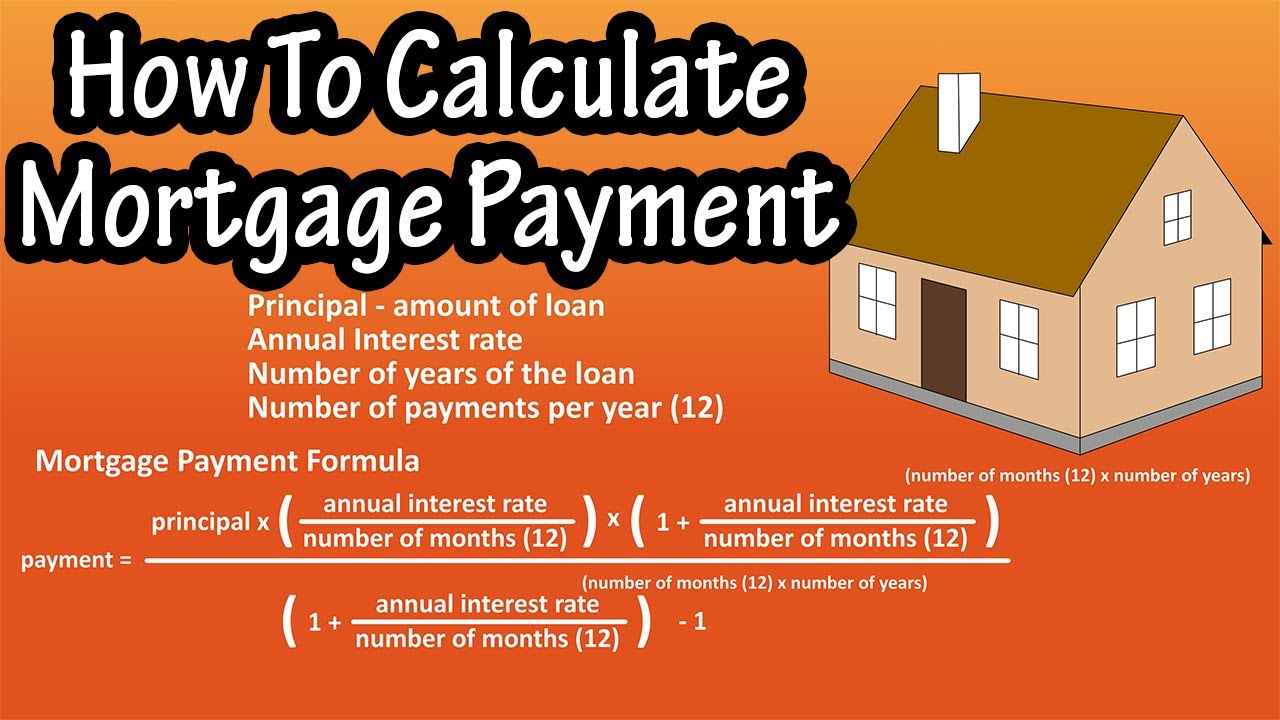

How to Calculate House Payment

Calculating your house payment can be done using a simple formula or an online mortgage calculator. Here’s how to do it:

The formula to calculate the monthly mortgage payment (M) is:

M = P[r(1 + r)^n] / [(1 + r)^n – 1]

Where:

- M = total monthly mortgage payment

- P = the principal loan amount

- r = monthly interest rate (annual rate / 12)

- n = number of payments (loan term in months)

For example, if you have a $300,000 mortgage with a 4% interest rate for 30 years, the calculation would be:

- Principal (P) = $300,000

- Monthly interest rate (r) = 0.04 / 12 = 0.00333

- Number of payments (n) = 30 x 12 = 360

Plugging these values into the formula gives you a monthly payment of approximately $1,432.25, excluding taxes and insurance.

Types of Mortgages

There are several types of mortgages that can affect your house payment:

- Fixed-Rate Mortgage: The interest rate remains the same throughout the loan term.

- Adjustable-Rate Mortgage (ARM): The interest rate can change after an initial fixed period.

- Interest-Only Mortgage: You only pay interest for a set period, after which you start paying principal.

Understanding Interest Rates

Interest rates play a significant role in determining your house payment. Here are some key points to consider:

- Higher interest rates increase your monthly payment.

- Shop around for the best rates from multiple lenders.

- A smaller rate difference can lead to substantial savings over the life of the loan.

Additional Costs Associated with Homeownership

In addition to your monthly mortgage payment, be aware of other costs that come with homeownership:

- Maintenance and Repairs: Regular upkeep is necessary to maintain property value.

- Utilities: Water, electricity, and gas are ongoing expenses.

- Homeowner Association (HOA) Fees: If applicable, these fees can add to your monthly costs.

Tips for Managing Your Mortgage

Managing your mortgage effectively can lead to financial stability. Here are some tips:

- Make extra payments when possible to reduce principal.

- Refinance if interest rates drop significantly.

- Set a budget to manage monthly expenses effectively.

Conclusion

In conclusion, understanding how to calculate house payment is essential for anyone looking to buy a home. By considering all the components, mortgage types, and additional costs, you can make informed decisions that benefit your financial future. Don't hesitate to engage with this information further—leave a comment, share this article, or explore additional resources on our site.

Thank you for reading! We hope this guide has helped you gain valuable insights into calculating your house payment and managing your mortgage effectively. We invite you to return for more informative articles and tips on navigating the world of homeownership.

Exploring The Life And Career Of Jordan Mason

Buc-ee's Near Me: The Ultimate Guide To Your Favorite Travel Stop

Taylor Swift Europe Tour: Everything You Need To Know

{kind=link}